25th February 2019

In January 2019, HM Government released their updated Environmental Reporting Guidelines - don’t worry if you’ve not heard about them, that’s why we’re here! This update includes streamlined energy and carbon reporting (SECR) guidelines which have been set up to supersede the CRC Energy Efficiency Scheme. However, this is not a like for like replacement as the SECR contains many significant changes and new reporting requirements to be paid attention to. But don’t worry, we’ve got your back. Here’s the key info you need to know.

If you were exempt from CRC, you may not be exempt from SECR. The updated guidelines require more businesses to comply than the CRC previously did, and your company may be one of them. SECR will mandate reporting for approximately 12,000 companies. It’s important to check to see if you qualify. To make this easier, we’ve listed the types of companies who will be affected below.

The guidelines aim to help companies and limited liability partnerships to comply with the Companies Act 2006 Regulations 2013, and the Companies and Limited Liability Partnerships Regulations 2018.

The SECR regulations will affect:

Large companies are defined by the Companies Act 2006 as those which have two or more of the following criteria for the reporting period:

Please note that you may fall within these categories, even if you are a not for profit or if you undertake public activities e.g. you are companies, registered companies or LLPs owned by universities, academies or NHS Trusts.

To those that these guidelines apply, these reporting guidelines are mandatory. Those companies to which these guidelines don’t apply, don’t fret, you’ve not been forgotten about! The guidelines have been written with the aim to support and encourage all other organisations to voluntarily report on a range of environmental matters, such as voluntary sustainability, energy and GHG emissions reporting.

There’s been changes made to Chapter One and Two of the guidelines, the remainder of the document has been left unchanged. The Government have provided steps to take when considering and reporting your environmental impact, as well as providing advice on which KPIs to report.

In the second chapter, the guidelines provide information regarding updated legal obligations and assistance on how to meet these obligations that come into force on 1st April 2019. This chapter has been had many of its sub-sections clarified and refined, such as the recommendation to disclose data in alignment with the Taskforce on Climate-related Disclosures principles, updated guidance on the “de minimis” provision for emissions and energy use reporting, and greater clarification on the types of organisations who are required to participate in SECR.

Other clarifications have been made in the following areas:

They also provide information on voluntary disclosures, to encourage businesses to go beyond SECR requirements. Advice is given about what additional voluntary information could be disclosed and which might prove beneficial for many organisations and a wide range of stakeholders.

Whatever you do, you must make sure the data you collect and report is relevant, quantitative, accurate, complete, consistent, comparable and transparent.

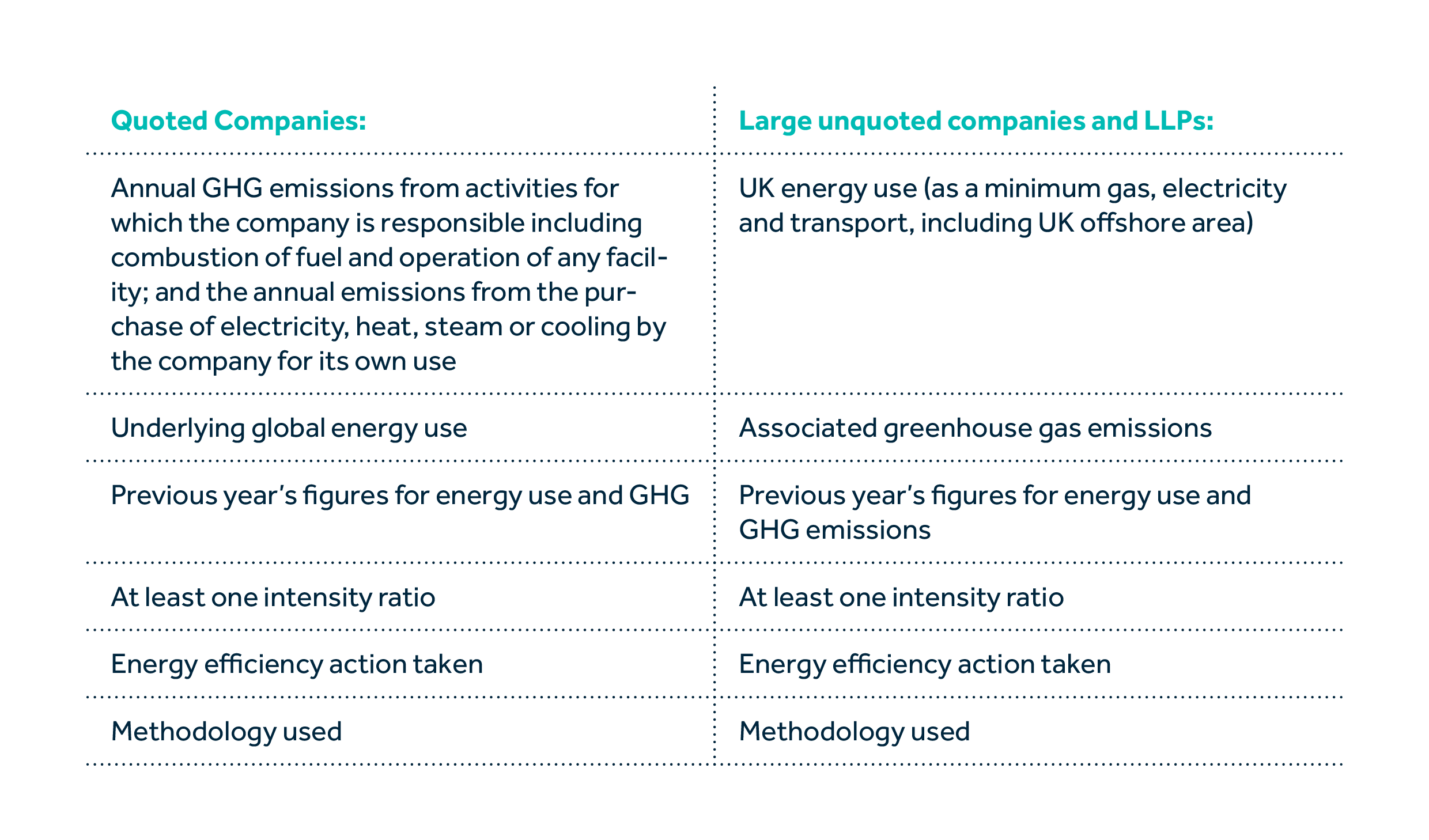

Below is the Government’s summary of the key obligations and scope of information that companies will need to report and disclose annually.

The new guidelines are set to come into force on 1st April 2019. This means that if your financial reporting year runs from April to March you’ll have to start gathering your data as early as April 2019. If it runs from January to December, then you must start gathering data from January 2020. Ideally, your environmental report should cover the same period as your financial year, and if it doesn’t, the environmental data collected should cover the majority of your financial year and a note should be made in the report to explain the discrepancy.

Start planning. If you’re unsure about whether these guidelines apply to you, it’s best that you assess your position as early as possible. If you have already done this before, all you’ll have to do is update your data collection methods to match the updated guidelines, and ensure that all the correct boxes are being ticked. If you’re new to this, don’t panic! You’ll find it useful to establish a process for data collection and calculation so that you are gathering the right data in the right way. When the time comes, you’ll be ready to report.

If you don’t need to comply with the guidelines, but want to stay ahead of the game with your environmental and sustainability reporting to protect your business against any future regulation amends that may require you to begin disclosing your data, then drop us a line. We can help you start your sustainability journey in a fuss free, professional way. We listen to your business to find out what matters most to you, where your biggest impacts are and what your long term business ambitions may be, and we create a unique sustainability action plan that is tailored specifically to you, with compliance factored in from the outset.

For more information on the Government’s Environmental Reporting updates, download the full PDF now.br>